Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Pradhan Mantri Suraksha Bima Yojana (PMSBY)

The Government of India launched several social security schemes to provide affordable insurance coverage for common citizens. Among the most popular and useful schemes are the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and the Pradhan Mantri Suraksha Bima Yojana (PMSBY).

These schemes aim to provide financial protection to families in case of death or disability at a very low premium. They are especially beneficial for middle-class families, low-income households, workers, and people without adequate insurance coverage.

In this article, we will try to understand:

- What is PMJJBY?

- What is PMSBY?

- Features and benefits

- Eligibility criteria

- Premium and coverage details

- Claim process

- Main differences between PMJJBY and PMSBY

- Frequently Asked Questions (FAQs)

What is Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)?

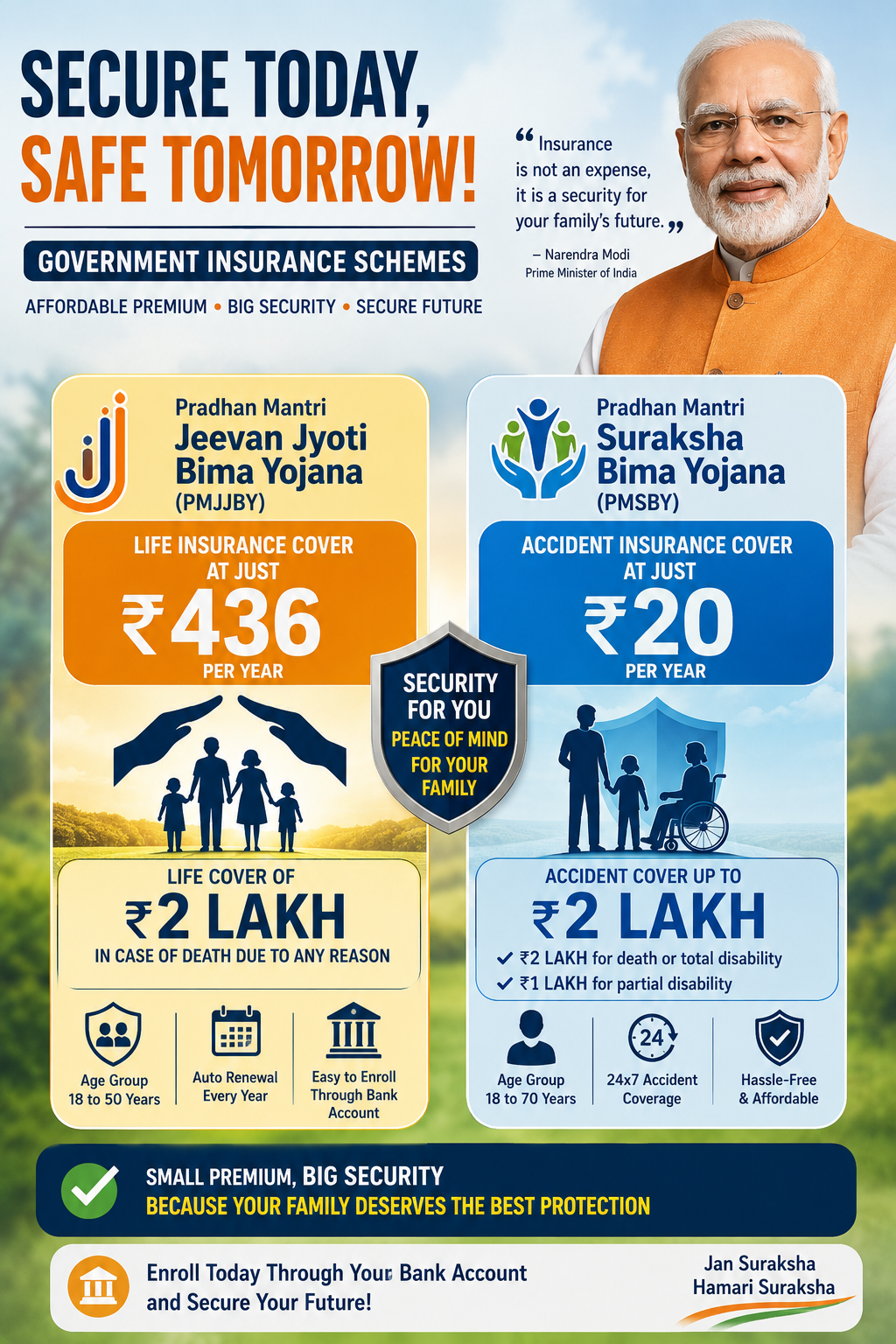

Pradhan Mantri Jeevan Jyoti Bima Yojana is a government-backed life insurance scheme launched in 2015.

It provides life insurance coverage in case of the insured person’s death due to any reason — natural or accidental.

The scheme is offered through banks and insurance companies and is linked to the subscriber’s savings bank account.

Key Features of PMJJBY

- Provides life insurance coverage of ₹2 lakh

- Covers death due to natural causes and accidents

- Very low annual premium

- Auto-debit facility from bank account

- Renewable every year

- Simple enrollment process

PMJJBY Coverage Details

| Particulars | Details |

|---|---|

| Insurance Coverage | ₹2 lakh |

| Annual Premium | ₹436.00 per year |

| Type of Insurance | Life Insurance |

| Coverage for Death | Natural + Accidental |

| Age Eligibility | 18 to 50 years |

| Policy Period | 1st June to 31 May |

| Bank Account Required | Yes |

Eligibility for PMJJBY

A person must fulfill the following conditions:

- Must be an Indian citizen

- Age should be between 18 and 50 years

- Must have a savings bank account

- Must consent to auto-debit of premium

Once enrolled before age 50, the person can continue the scheme up to age 55 by paying the premium annually.

Benefits of PMJJBY

1. Affordable Life Insurance

PMJJBY offers ₹2 lakh life insurance at a very low premium, making it affordable for almost everyone.

2. Covers Natural Death

Unlike many accidental policies, PMJJBY also covers death due to illness or natural causes.

3. Financial Support for Family

In case of the policyholder’s death, the nominee receives the insurance amount, which can help the family manage expenses.

4. Easy Enrollment

The scheme can be activated directly through banks, internet banking, or mobile banking.

What is Pradhan Mantri Suraksha Bima Yojana (PMSBY)?

Pradhan Mantri Suraksha Bima Yojana is a government-backed accident insurance scheme launched in 2015.

It provides financial protection against accidental death and disability.

The scheme is especially useful for workers, daily wage earners, travelers, and people exposed to physical risks.

PMSBY Coverage Details

| Particulars | Details |

|---|---|

| Insurance Coverage | ₹2 lakh |

| Annual Premium | ₹20 per year |

| Type of Insurance | Accident Insurance |

| Coverage | Accidental Death & Disability |

| Age Eligibility | 18 to 70 years |

| Policy Period | 1 June to 31 May |

| Bank Account Required | Yes |

Disability Benefits under PMSBY

| Condition | Insurance Benefit |

|---|---|

| Accidental Death | ₹2 lakh |

| Total Permanent Disability | ₹2 lakh |

| Partial Permanent Disability | ₹1 lakh |

Examples of Permanent Disability

- Loss of both eyes

- Loss of both hands or feet

- Loss of one eye and one limb

- Permanent disability due to an accident

Eligibility for PMSBY

To enroll in PMSBY:

- The person must be between 18 and 70 years old

- Must have a savings bank account

- Must agree to auto-debit of premium

Benefits of PMSBY

1. Extremely Low Premium

At just ₹20 annually, PMSBY is one of the cheapest insurance schemes available in India.

2. Accident Protection

It provides financial help in case of accidental death or disability.

3. Useful for Workers and Travelers

People involved in physical work or frequent travel can benefit greatly from this scheme.

4. Easy Claim Settlement

The process is simple and supported by banks and insurance companies.

Main Differences Between PMJJBY and PMSBY

| Feature | PMJJBY | PMSBY |

|---|---|---|

| Full Form | Pradhan Mantri Jeevan Jyoti Bima Yojana | Pradhan Mantri Suraksha Bima Yojana |

| Type of Insurance | Life Insurance | Accident Insurance |

| Coverage Amount | ₹2 lakh | ₹2 lakh |

| Premium | ₹436/year | ₹20/year |

| Coverage Type | Death due to any reason | Accidental death/disability |

| Natural Death Covered? | Yes | No |

| Accidental Death Covered? | Yes | Yes |

| Disability Coverage | No | Yes |

| Entry Age | 18–50 years | 18–70 years |

| Maximum Coverage Age | 55 years | 70 years |

| Best For | Family financial protection | Accident risk protection |

Can You Take Both PMJJBY and PMSBY?

Yes. In fact, experts often recommend taking both schemes together because:

- PMJJBY provides life cover for all types of death

- PMSBY provides accident and disability cover

- Combined annual premium is very low

Total Annual Premium for Both Schemes

| Scheme | Premium |

|---|---|

| PMJJBY | ₹436 |

| PMSBY | ₹20 |

| Total | ₹456 per year |

For less than ₹500 annually, a person can get significant financial protection.

How to Enroll in PMJJBY and PMSBY

You can enroll through:

- Public sector banks

- Private banks

- Internet banking

- Mobile banking apps

- Bank branches

Documents Required

- Aadhaar Card

- Savings Bank Account

- Mobile Number

- Consent for auto-debit

Claim Process for PMJJBY

Step-by-Step Process

- Inform the bank or insurance company

- Submit the claim form

- Submit the death certificate

- Provide nominee details and bank account

- Verification by insurer

- Claim amount transferred to the nominee

Claim Process for PMSBY

Required Documents

- Claim form

- FIR or accident report (if applicable)

- Disability certificate or death certificate

- Bank account details

After verification, the insurance amount is credited to the beneficiary.

Important Limitations of PMJJBY and PMSBY

PMJJBY Limitations

- Coverage amount may not be sufficient for large financial needs

- Policy lapses if bank balance is insufficient for premium deduction

PMSBY Limitations

- Only accident-related claims are covered

- No benefit for illness-related hospitalization or death

Why These Schemes Are Important

These schemes promote:

- Financial inclusion

- Insurance awareness

- Social security for low-income families

- Affordable protection for rural and urban citizens

Millions of Indians who could not afford expensive insurance policies now have access to basic insurance protection through these schemes.

Frequently Asked Questions (FAQs)

1. Is Aadhaar mandatory for PMJJBY and PMSBY?

Aadhaar is generally preferred for KYC purposes, though banks may accept other valid documents.

2. Can a person have multiple PMJJBY or PMSBY accounts?

No. A person can enroll only once under each scheme.

3. What happens if the bank balance is insufficient?

The policy may lapse if the premium cannot be auto-debited.

4. Can NRIs join these schemes?

Yes, NRIs with eligible bank accounts in India can enroll, subject to scheme conditions.

5. Is a tax benefit available?

Premiums may qualify for tax benefits under applicable sections of the Income Tax Act.

Conclusion:

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Pradhan Mantri Suraksha Bima Yojana are two excellent government-backed insurance schemes designed to provide affordable financial protection to middle-class and lower-class Indian citizens.

While PMJJBY offers life insurance coverage for death due to any reason, PMSBY focuses on accidental death and disability protection. Since both schemes are available at extremely low premiums, they can play an important role in securing the financial future of families.

For individuals looking for basic insurance protection at minimal cost, enrolling in both schemes can be a smart financial decision.

Readers will also like to read blogs on the following topics

3. Basics of the Future and options

4. PE Ratio

6. Bull vs Bear Phase in the Stock Market

7. XIRR vs CAGR vs Absolute Return

8. Home