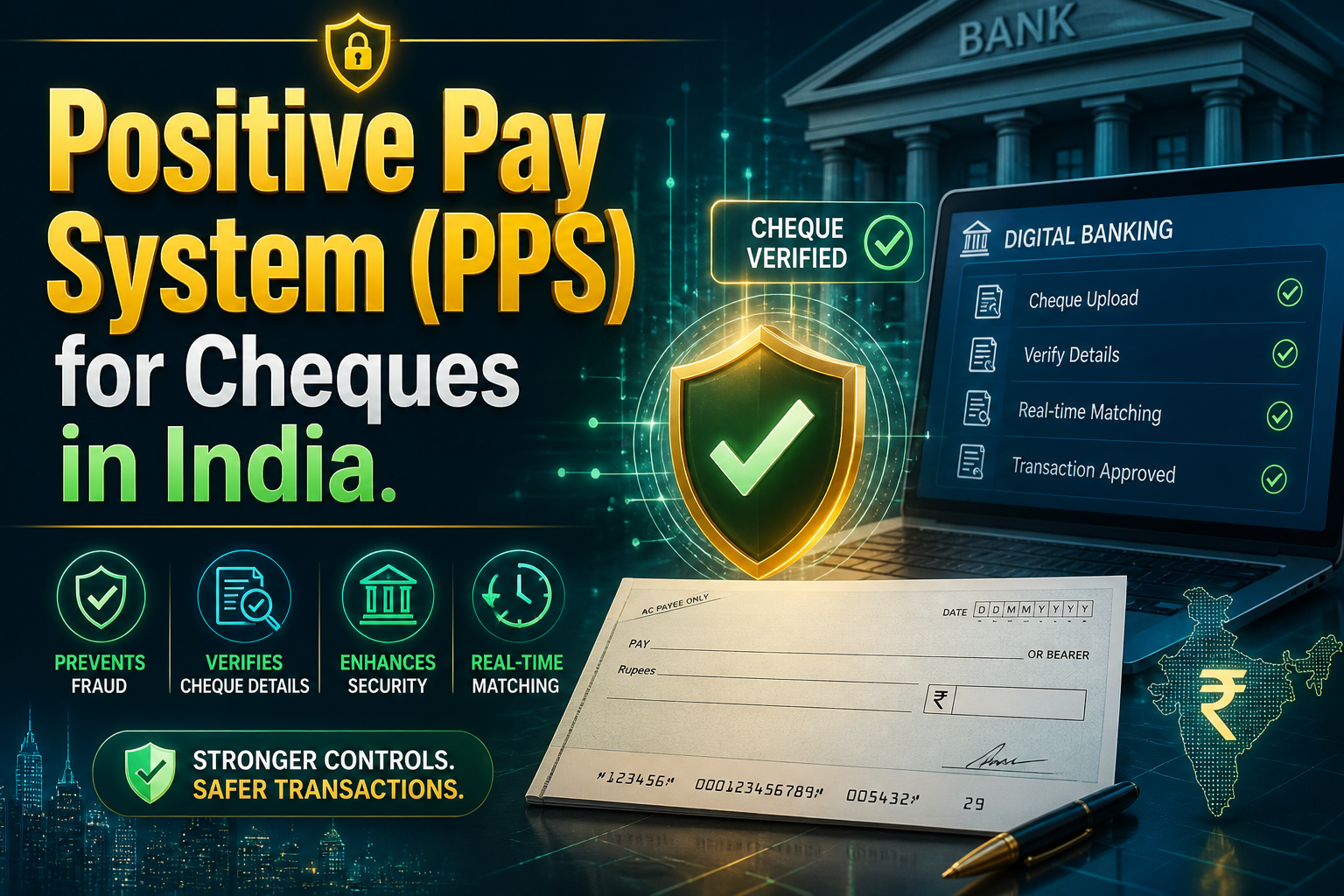

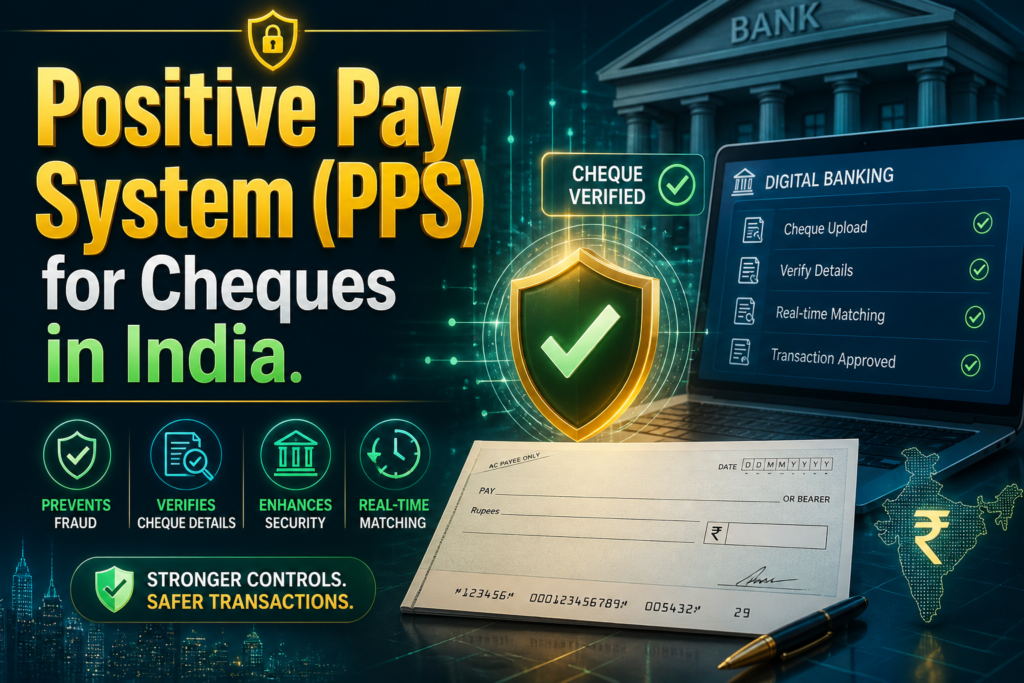

What is Positive Pay System (PPS) for Cheques: Its Limit, Process & How Does It Work

Nowadays in India, digital payments are widely used. But some people still use cheques for high-value payments. Cheque-related fraud has also increased. This prompted the Indian Banking system to take stronger security measures. One such important initiative is the Positive Pay System (PPS) introduced by the Reserve Bank of India.

This blog article explains everything you need to know about PPS—its meaning, limit, process, benefits, and how it works.

What is Positive Pay System (PPS)?

The Positive Pay System (PPS) is a fraud prevention mechanism for cheque payments. Under this system, the cheque issuer (drawer) must share key details of the cheque with their bank before it is presented for clearing.

When the cheque is presented, the bank cross-verifies the details with the information already provided. If everything matches, the cheque is cleared. If not, it may be flagged or rejected.

Simply put, PPS acts as a double verification layer for cheque payments.

Why Was PPS Introduced?

Cheque frauds like:

- Alteration of the cheque amount

- Forged signatures

- Changes in payee name

have been major concerns in India.

To reduce such risks, the Reserve Bank of India introduced PPS under the Cheque Truncation System framework.

What is the PPS Limit?

Initially, PPS was made mandatory for cheques of ₹50,000 and above. However:

- Banks may offer PPS for lower amounts as well

- Some banks encourage PPS for all cheque values

For high-value cheques (₹50,000+), PPS is strongly recommended to avoid delays or rejection.

Key Details Required in PPS

Before issuing the cheque, the Cheque issuer must provide the following details to the bank:

- Account number

- Cheque number

- Cheque date

- Payee name

- Amount

- Optional: Image of the cheque (front & back)

How Does the Positive Pay System Work?

Step-by-Step Process:

1. Issuing the Cheque

The account holder writes a cheque as usual.

2. Submitting Cheque Details

The issuer submits cheque details through:

- Net banking

- Mobile banking

- SMS banking

- ATM (in some banks)

- Branch visit

3. Data Storage by Bank

The bank securely stores these details in its system.

4. Cheque Presentation

The payee deposits the cheque for clearing.

5. Verification

The bank matches:

- Cheque amount

- Payee name

- Cheque number

- Date

6. Clearance or Flagging

- ✔ If details match → cheque cleared

- ❌ If mismatch → flagged or rejected

How to Register for PPS?

Most banks in India allow PPS registration through:

- Internet banking portal

- Mobile banking app

- SMS facility

- Physical form submission

Example: Many banks provide a “Positive Pay” option under Cheque Services.

Benefits of the Positive Pay System

1. Fraud Prevention

Prevents tampering and unauthorized changes.

2. Safer High-Value Transactions

Adds an extra layer of security for large payments.

3. Faster Dispute Resolution

Mismatch detection helps in quick investigation.

4. Increased Customer Confidence

Users feel more secure using cheques.

What Happens if PPS is Not Used?

If PPS details are not submitted for high-value cheques:

- The cheque may still be processed, but

- Banks may exercise extra caution

- It could result in:

- Delayed clearance

- Additional verification

- Possible rejection in case of suspicion

Important Points to Remember

- PPS is not mandatory for all cheques, but recommended

- Especially useful for ₹50,000+ transactions

- Details must be submitted before cheque presentation

- Even a small mismatch can lead to rejection

Real-Life Example

Suppose you issue a cheque of ₹1,00,000:

- You submit details via mobile banking

- The payee deposits the cheque

- Bank compares data with submitted details

- If everything matches → cleared smoothly

- If the amount is altered → cheque rejected

Conclusion

The Positive Pay System (PPS) is a crucial step towards making cheque transactions safer in India. Introduced by the Reserve Bank of India, it significantly reduces fraud risks by ensuring that cheque details are verified before clearance.

While digital payments are growing, cheques still play an important role—especially in business and high-value transactions. Using PPS ensures that these transactions remain secure, reliable, and trustworthy.

Frequently Asked Questions.

1. Is PPS mandatory for all cheques?

No, but it is highly recommended for cheques above ₹50,000.

2. Can PPS be done after issuing the cheque?

Yes, but it must be done before the cheque is presented for clearing.

3. Is there any charge for PPS?

Most banks provide PPS free of cost.

4. Can I cancel PPS details?

Yes, you can modify or cancel before cheque presentation.

Readers will also like to read blogs on the following topics

3. Basics of the Future and options

4. PE Ratio

6. Bull vs Bear Phase in the Stock Market

7. XIRR vs CAGR vs Absolute Return

8. Home