What is CKYCR Number?

The Centralized KYC Registry (CKYCR) is one of the most important reforms in India’s financial system. It allows the customer to complete KYC only once. The customer can then reuse it across any financial institution. In this blog, we will detail the procedure for creating CKYCR, its usage across banks, and its advantages.

Full form of CKYCR is Centralized KYC Registry

What is Centralized KYC Registry (CKYCR)?

The Central KYC Registry (CKYCR) is a centralized repository that stores the KYC details of customers in a digital format. It is managed by the Central Registry of Securitisation Asset Reconstruction and Security Interest (CERSAI). It is authorised by the Government of India.

Once a customer completes KYC with any financial institution, the data is uploaded to this registry, and a unique 14-digit CKYC number (KIN) is generated.

This number acts as a universal identity for financial transactions, eliminating the need to repeat the submission of KYC documents.

Why CKYC Was Introduced

CKYC is introduced to avoid the repeated submission of KYC documents to various financial institution like Bank accounts, mutual fund investments, Insurance policies, and Demat accounts. It also speeds up the overall processing time and reduces duplication, delays, and inefficiency in the system.

CKYC was introduced under the Prevention of Money Laundering Act (PMLA), 2002, to:

- Standardize KYC across institutions

- Reduce fraud and money laundering

- Improve efficiency in onboarding customers

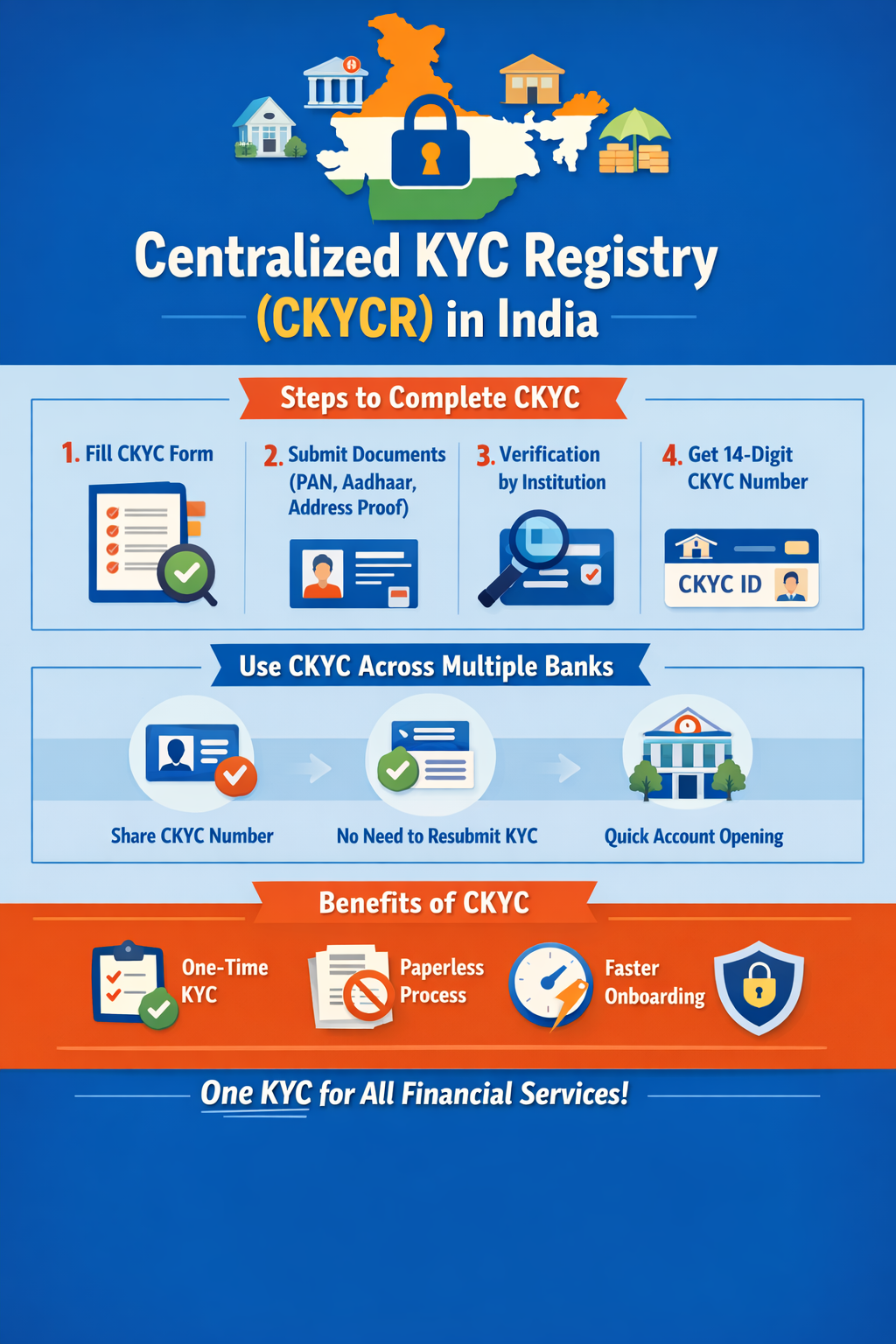

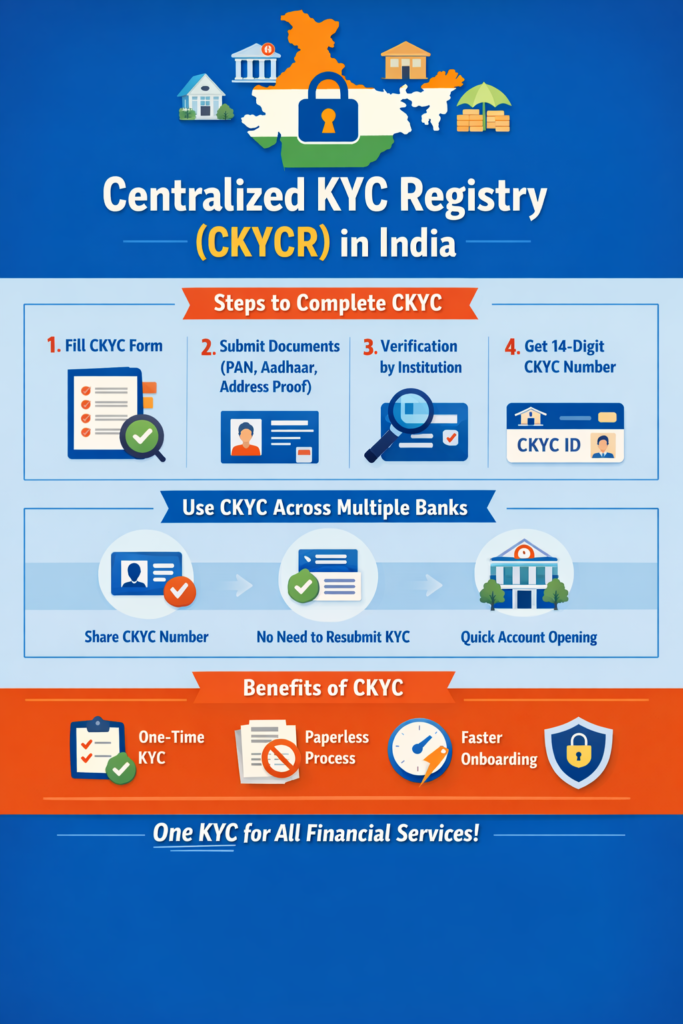

Detailed Procedure to Complete CKYC in India

Completing CKYC is simple and can be done through any financial institution, such as banks, mutual fund companies, or insurance providers.

Step 1: Visit a CKYC-Registered Institution

Go to any of the following:

- Bank branch

- Mutual fund house (AMC)

- Insurance company

- Stock broker

These entities are authorized by regulators like RBI, SEBI, IRDAI, and PFRDA.

Step 2: Fill the CKYC Form

You need to fill out a standard CKYC form, which includes:

- Name

- Date of birth

- Address

- PAN/Aadhaar details

- Contact information

Step 3: Submit Documents

Proof of Identity (POI)

- PAN card

- Aadhaar

- Passport

- Voter ID

Proof of Address (POA)

- Aadhaar

- Utility bill

- Bank statement

- Passport

Also submit:

- Passport-size photograph

- Signature

Step 4: Verification Process

The institution verifies your documents:

- Aadhaar is verified via UIDAI

- PAN is validated with the Income Tax database

This ensures the authenticity of your data.

Step 5: Upload to CKYCR

After verification:

- Your KYC data is uploaded to CKYCR

- If you don’t already have CKYC, a new record is created

Step 6: CKYC Number Generation

You receive a 14-digit CKYC number (KIN) via:

- SMS

- Bank communication

This number is your permanent KYC identity.

Step 7: Check CKYC Status

You can check your CKYC status:

- Online via CKYC portal

- Through your bank

- Using PAN or CKYC number

Types of CKYC Accounts

Depending on documents submitted, CKYC accounts are classified as:

- Normal Account – Full KYC with valid documents

- Simplified Account – Limited documentation

- Small Account – Minimal KYC, restricted usage

- OTP-based eKYC – Aadhaar OTP-based verification

How to Use CKYC Across Multiple Banks

One of the biggest advantages of CKYC is interoperability.

Step-by-Step Usage:

- Provide CKYC Number

- While opening a bank account or investing, just share your CKYC number

- Institution Fetches Data

- The bank accesses your KYC details from CKYCR

- No Document Submission Required

- No need to submit PAN, Aadhaar, or address proof again

- Faster Account Opening

- Instant or near-instant onboarding

- Automatic Updates

- Any change in your KYC (address, mobile number) is updated across institutions

Example:

If you completed CKYC while opening an account in Bank A, you can open an account in Bank B or invest in a mutual fund just by providing your CKYC number.

Institutions Where CKYC Can Be Used

CKYC works across all major financial sectors:

- Banks

- NBFCs

- Mutual Funds

- Insurance Companies

- Stock Brokers

This makes CKYC a universal KYC system in India.

Advantages of CKYC

1. One-Time KYC

You only need to complete KYC once for all financial services.

2. No Repetitive Paperwork

Eliminates repeated submission of documents for every new investment or account.

3. Faster Account Opening

Financial institutions can instantly access verified data, reducing onboarding time.

4. Universal Acceptance

CKYC is accepted across:

- RBI-regulated entities

- SEBI-regulated institutions

- IRDAI and PFRDA entities

5. Digital & Paperless Process

Promotes a fully digital ecosystem with minimal paperwork.

6. Centralized Data Storage

All your KYC data is stored securely in one place and accessible when required.

7. Easy Updates

Update your KYC once, and changes reflect across all institutions.

8. Improved Security

- Encrypted storage

- Access only to authorized institutions

- Reduced fraud risk

9. Regulatory Compliance

Helps in preventing:

- Money laundering

- Fraudulent financial activities

10. Convenience for Investors

Especially beneficial for:

- Mutual fund investors

- Stock market participants

- Insurance buyers

Limitations of CKYC

While CKYC is highly beneficial, it has some limitations:

- Not all legacy accounts are CKYC-compliant

- Updates may take time to reflect

- Some institutions may still ask for additional verification

Future of CKYC in India

India is moving toward a Universal KYC system with enhanced integration. Recent developments indicate:

- CKYC Registry 2.0 with DigiLocker integration

- Faster updates and digital verification

This will further simplify onboarding and improve user experience.

Conclusion

The Centralized KYC Registry (CKYCR) is a game-changer in India’s financial system. By enabling “One KYC for all financial services”, it reduces paperwork, saves time, and enhances security.

For investors and banking customers, completing CKYC is no longer optional—it is a smart step toward seamless financial transactions. Once you have your CKYC number, you unlock a fast, paperless, and hassle-free financial journey across banks, mutual funds, and insurance companies.

Key Details

- The CKYC system is managed by CERSAI (Central Registry of Securitisation Asset Reconstruction and Security Interest of India) under the Ministry of Finance.

- The portal ckycindia.in is the official platform where:

- Financial institutions upload your KYC data

- You can check your CKYC status

- You can download your CKYC (KIN) card

Important Clarification

? You cannot directly create CKYC yourself on the website.

- CKYC is generated only when you complete KYC through a bank, mutual fund, or financial institution

- These institutions upload your details to the CKYC portal

- After verification, you receive your 14-digit CKYC number (KIN)

What You Can Do on the CKYC Website

On the official portal, you can:

- Check CKYC status

- Download CKYC ID/card

- Access FAQs and updates

- Verify if your KYC is already registered

Summary

- ✅ Official website: ckycindia.in

- ✅ Managed by: CERSAI (Government of India)

- ❌ You cannot apply directly online

- ✅ CKYC is created via banks/financial institutions

Readers will also like to read blogs on the following topics

3. Basics of the Future and options

4. PE Ratio

6. Bull vs Bear Phase in the Stock Market

7. XIRR vs CAGR vs Absolute Return

8. Home